Investing for tomorrow, because Energy subsidies will decline 25% by 2050 – analysis

IRENA has modelled energy subsidies to 2030 and 2050 for their pathway to meet the Paris targets. Here, Michael Taylor summarises their findings. Firstly, they estimate today’s global direct energy sector subsidies to be $634bn/year (2017 figures). The vast majority, $447bn, went to fossil fuels. (By the way, he points out that none of these figures include the externality costs – pollution, healthcare, environment – which equate to trillions and would surely be cut substantially by each step taken towards decarbonisation). Total direct energy sector subsidies will decline by 25% by 2050, mostly thanks to cuts to support for those fossil fuels. The other clean energy categories will increase their share of the smaller total, and as their costs evolve so too do their required subsidy as efficiencies, cost reductions, and growing demand register. Taylor looks at renewable power generation, energy efficiency, buildings, renewable heat, nuclear, electric vehicles and more. Given the current crisis, he stresses that governments now needing to stimulate their economies should prioritise the energy sector: though poorly understood in the mainstream media, the clean energy transition was always designed to cut medium to long term costs, just like the best stimulus packages should do.

In these exceptional times, as the COVID19 pandemic has resulted in far reaching impacts on societies and the economy, governments are rightly focused on managing the public health emergency and protecting their citizens. Although the world is, undoubtedly, going to need to manage this pandemic over the months and even years ahead; there will come a point where restrictions on the economy can be relaxed – in a way consistent with minimising the risk of the virus – and governments and policy makers around the world will turn to the next phase – recovery and growth.

When that time comes, policy makers will be looking at how to design a stimulus that can be rapidly scaled up, boost the flow of money in the real economy, create good-quality jobs and provide the basis for long-term economic growth and recovery that mitigates the economic harm done to the average citizen during this exceptional public health emergency. This stimulus when it comes is an opportunity for economies to invest in infrastructure and people that will boost the long-term prospects for sustainable growth, that also make the economy more resilient to the crises of the future. IRENA’s recently released Global Renewables Outlook, highlights a pathway to a sustainable energy future that identifies a range of potential investment opportunities, consistent with a green stimulus.

The cost of subsidies matter now more than ever

The contraction in economic activity caused by the lockdowns, necessary to contain the spread of the virus, and the corresponding additional government spending in relief packages to individuals, small businesses and crucial sectors of the economy is going to result in larger public sector deficits and borrowing over the short-term. The formulation of stimulus packages will therefore be influenced by the reduced fiscal margin for maneuver in many countries. Programmes’ abilities to generate jobs and boost long-term productivity growth will also be benchmarked against the fiscal affordability of the policies needed to support some stimulus spending.

Energy subsidy projections for the transition: trending down, not up

In this respect, recent analysis by the International Renewable Energy Agency sheds some light on the general affordability of the energy transition (in terms of macroeconomic impacts) and also the evolution of energy subsidies in the energy sector. This is useful, because the acceleration of the energy transition requires a scaling-up of investments in a wide range of areas from innovation in electrolysers, to heat pumps, to the use of alternative fuels in transport. But what they all have in common is an increase in investment over recent trends, effectively a stimulus to the real economy through greater investment in energy supply infrastructure and end-use technologies.

The macro-economic argument over the longer-term of the energy transition is compelling, with a payback of USD 3 to USD 8 for every dollar invested. However, as already noted the potential medium-term strain on public finances may impose constraints that might mean the optimal choices are not possible.

IRENA’s recent analysis of the evolution of energy sector subsidies in the energy transition, however, given reason to be optimistic that this will not be a constraint on ensuring the coming stimulus packages can be green, as well as good for jobs and the economy.

Current subsidy breakdown

Before looking at how energy sector subsidies evolve over the medium- to long-term, it’s worth noting that differing boundary conditions and accounting methodologies for energy subsidy calculation mean there is some confusion around what the exact level of energy sector subsidies actually are.

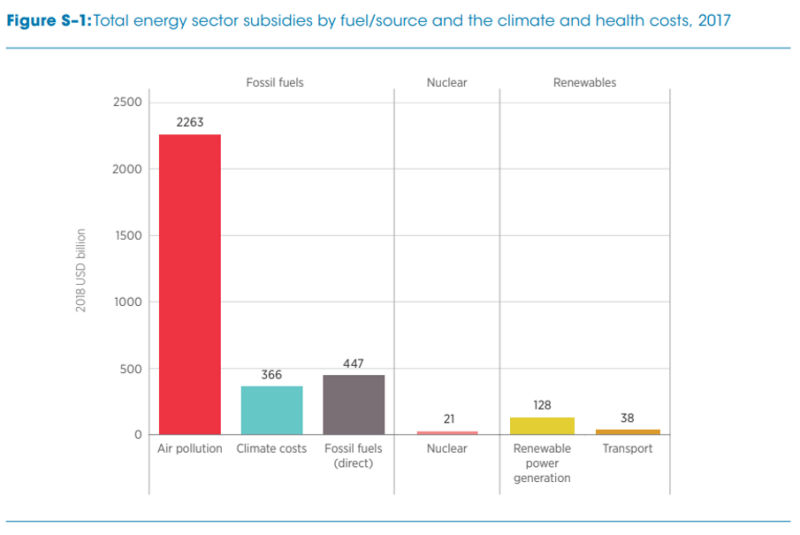

By combining analysis from a number of existing sources, IRENA has estimated direct energy sector subsidies to be, at least, USD 634 billion in 2017 (Figure 1). Of the total, USD 447 billion was attributable to fossil fuels, USD 128 billion to renewable power, USD 38 billion renewable transport (predominantly biofuels) and a placecholder estimate of USD 21 billion for nuclear in the absence of comprehensive global data. However, if the unpriced externality costs from fossil fuels are considered, the total rises significantly to USD 3.1 trillion.

Total subsidies lower in 2030, 2050

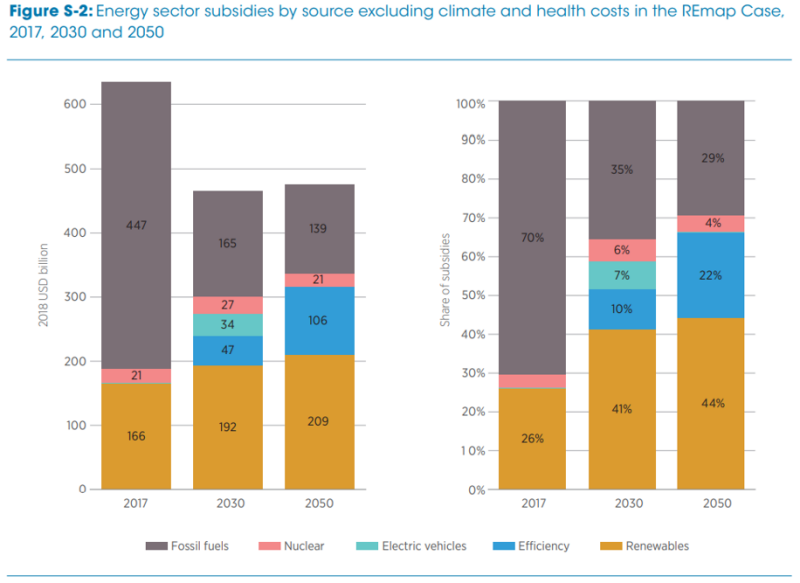

IRENA has used the analysis in the REmap Case (IRENA, 2020), in conjunction with the current estimates of total energy sector subsidies in 2017, to analyse how total energy sector subsidies out to 2050 might evolve if the world is to stay on track to achieve the Paris Agreement climate goal of restricting global warming to 2 °C or less. The analysis assumes that today’s fossil fuel subsidies would be rapidly reduced by 2030, but not entirely phased out by 2050.

The results show that between 2017 and 2030, total annual energy sector subsidies could decline from USD 634 billion to USD 466 billion per year, according to the REmap Case for the realistic acceleration in the worldwide deployment of renewables, and they would rise slightly to be around USD 475 billion in 2050 (Figure S-2). Total energy sector subsidies in 2050 would therefore be around 25 % lower than in 2017 and 45 % (USD 390 billion) lower than they would be based on a business-as-usual scenario.

This is before considering the reduction in the implicit subsidies from unpriced externalities, which could be reduced by between USD 620 billion to USD 2 160 billion relative to the Reference case in 2030 and between USD 2.5 trillion and USD 6.3 trillion in 2050.

Fossil fuel subsidies decline significantly

Direct subsidies for fossil fuels fall from USD 447 billion in 2017, to USD 165 billion in 2030 and to USD 139 billion in 2050 in the REmap Case, as per unit subsidies are reduced and fossil fuel demand declines. Existing subsidy programmes are reduced significantly and by 2050 over 90 % of the subsidies to fossil fuels are to support carbon dioxide capture and storage (CCS) in industrial applications.

Other subsidies increase, but evolve

As renewable power becomes increasingly competitive and early high-cost subsidies to solar PV, in particular, expire, the subsidies for renewable power generation decline to USD 53 billion in 2030 and are virtually eliminated by 2050, according to REmap projections.

With more effort to decarbonise the more difficult end-use sectors, their share of subsidies begins to increase. The subsidies needed over and above the Reference Case in Industry by 2050 reach USD 166 billion, with USD 100 billion for energy efficiency and the balance for renewable heat. In the Buildings sector, subsidies grow to USD 28 billion in 2050, predominantly (88 %) for renewable heating, cooling and cooking solutions.

EU outlook

The pattern in the European Union is similar to the global outlook: support needs to renewable power generation will peak before 2030, with the ongoing cost declines for solar and wind power technologies.

In the transport sector, the remarkable declines in electric vehicle (EV) battery pack costs mean decarbonisation, in conjunction with an increasingly renewables dominated power generation system, will not require the large subsidies that were required to drive down costs in solar and wind. Subsidies will rise, however, in the buildings and industrial sectors, notably between 2030 and 2050, as these more difficult to decarbonise sectors are tackled.

Overall, the energy transition can be consistent with lower subsidies in the energy sector and significant long-term economic benefits. Incorporating renewables and energy efficiency in stimulus packages is not only consistent with the short-term goals of stimulating investment in the real economy, creating quality jobs, and fostering long-term, resilient economic growth; but should not exacerbate medium-term fiscal challenges.

***

Michael Taylor is a Senior Analyst at IRENA

References

IRENA (2020a), Global Renewables Outlook: Energy Transformation to 2050, IRENA, Abu Dhabi

IRENA (2020b), Energy subsidies: Evolution in the global energy transformation to 2050, IRENA, Abu Dhabi

www.irena.org\publications

Source: https://energypost.eu/investing-for-tomorrow-because-energy-subsidies-will-decline-25-by-2050-analysis/